Join day by day information updates from CleanTechnica on e-mail. Or observe us on Google Information!

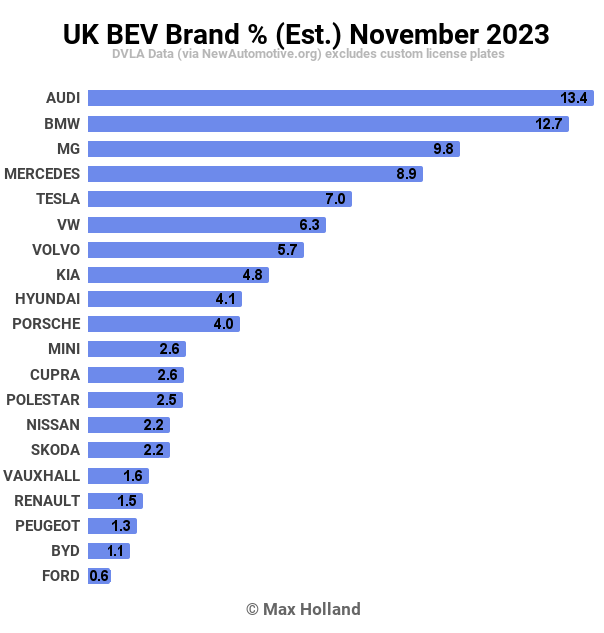

November noticed the UK EV share at 25.7% of the auto market, down from 27.7% YoY. Plugin hybrid volumes grew by 56% YoY, while full electrical volumes fell by 17%, probably a hold-back forward of incoming coverage modifications. General auto quantity was 156,525 models, up 9.5% YoY, roughly in step with pre-2020 seasonal norms. Audi was the UK’s greatest promoting BEV model in November.

November’s market noticed UK mixed EV share at 25.7%, comprising 15.6% full electrics (BEVs), and 10.1% plugin hybrids (PHEVs). These examine with YoY shares of 27.7%, with 20.6% BEV, and seven.1% PHEV.

We will see that PHEVs are up, however that BEV share is notably down yr on yr. Even in opposition to an general market YoY development of 9.5%, BEV quantity fell by over 17%, a really uncommon sample.

The SMMT claims that the November 2022 baseline for the YoY comparability was unusually excessive for BEVs, however the knowledge doesn’t assist this in any respect. As an alternative, the information exhibits that the 2022 finish of yr uptick was carefully in step with the pattern that the UK additionally noticed on the finish of 2020, and 2021, together with the top of yr pattern in nearly each different European market.

A extra possible motive why this yr’s finish of yr share shouldn’t be seeing the standard uptick within the UK, is the upcoming arrival of tighter “ZEV mandate” rules ranging from January 1st 2024. Extra on this within the outlook part beneath. Suffice it to say that many producers are possible now holding again a few of their late-2023 deliveries till 2024, to assist them meet the primary yr necessities of the incoming ZEV mandate.

On condition that November and December will likely be distorted by this strategic hold-back, there’s not rather more to say concerning the actual numbers we are actually seeing. Fortunately, diesel-only share continues to fall off, at a file low of three% in November.

Finest Promoting Manufacturers

Tesla was unusually low on deliveries for the second month of 1 / 4, possible additionally associated to the incoming ZEV mandate. Their November 2023 quantity was just one,599 models, whereas their typical second-month-of-quarter quantity over the previous yr has been greater than 3,000, and their earlier two Novembers each noticed over 4,000 models.

Audi was joyful to step into the hole, taking November’s lead spot, taking 13.4% of the UK BEV market, forward of acquainted faces, BMW and MG.

As a result of imminent ZEV mandate, and producers strategizing their UK deliveries in relation to it, I’m not going to analyse strikes in a lot element this month, since they’re ephemeral.

We should always, nevertheless, notice BYD’s strongest UK month to this point, with 267 models, comprising the Atto 3 and the Dolphin. BYD’s UK supply batching remains to be a bit patchy for now, however will little question even out because the model turns into extra established within the nation. BYD is competing with MG for one of the best worth BEV spot, however has a protracted approach to go to match MG’s volumes.

Let’s take a look at the three month image:

Tesla nonetheless maintains its lead, although at a a lot diminished hole over others, since its quantity is simply 71% that of the prior interval. All the opposite high 20 manufacturers grew their quantity over the identical interval, aside from Polestar and Vauxhall.

The approaching few months within the UK BEV market will likely be messy, however we will likely be right here to map it.

Outlook

Past the auto market’s affordable well being, the UK financial system stays weak, with newest GDP YoY development remaining at 0.6%. Inflation has decreased to 4.6%, and rates of interest are flat at 5.25%. Manufacturing PMI elevated to 47.2 factors in November from 44.8 factors in October.

As for the BEV outlook, the market faces disjunctions. The brand new ZEV mandate, beginning in 2024, requires auto producers to promote roughly 22% ZEVs (i.e. BEVs) within the UK, or face stiff fines. The precise numerical requirement is a little more sophisticated — a politically fudged system, designed to maintain laggards like Ford, Honda and Toyota from following via on their threats to tug out of their UK factories and associated investments.

Holding again what ought to be late-2023 buyer deliveries of BEVs, and delaying these deliveries till January 2024, provides producers a head begin on assembly this new 2024 requirement.

The SMMT, being the trade physique, is on the aspect of the producers on this. That is possible why the SMMT’s most up-to-date market report is attempting to give you diversionary explanations for why BEV shares are at the moment down YoY. They are saying “final November [2022] was atypical with vital deliveries following provide chain disruptions.” Sorry SMMT, however that’s not an correct account.

I’d count on even Tesla to have some extent of supply hold-back within the UK for the rest of 2023. Why? As a result of there will likely be a ZEV credit buying and selling scheme whereby Tesla, Polestar, and different producers which are forward of the curve, can become profitable from the laggard producers. If Tesla needs to fulfill specific 2023 international year-end supply targets, they may extra possible strive to do this by way of different European markets and elsewhere.

The opposite producers whose UK gross sales steadiness is already comparatively BEV-heavy embrace: Porsche, MG, BMW, Audi, Mercedes-Benz, Cupra, and Volvo. All are already above or shut to twenty% BEV.

These producers and types that are inside attain of the 2024 requirement (with a little bit of arduous work) embrace the Korean manufacturers, Volkswagen, Audi, a lot of the Stellantis manufacturers, and maybe Renault.

Nissan will want an almighty effort. Ford and the remaining Japanese manufacturers don’t have any likelihood, and must juggle the system, and purchase credit from others, and borrowing from their future selves. Not kidding, the political fudge permits deferred accounting, at the least till the top of 2026.

Low quantity manufacturers (Ferrari, McLaren, and so forth) get a brief cross, however they too must step up earlier than the top of the last decade. To study extra concerning the imminent UK ZEV scheme, there’s a helpful overview by Phil Curry, over at Autovista24.

What we will predict is that the general market will see BEVs at the least at 22% share in 2024. The mandate thereafter steadily ramps up, to 38% by 2027, after which extra steeply, to 80% by 2030.

I count on the transition may occur rather a lot sooner than this deliberate timeline, until UK political actors block the import of great-value Chinese language BEVs from the likes of Tesla, MG and BYD, which they could, relying on stress from the Neo-Cons and Chilly Warriors.

What are your ideas on the UK’s transition to EVs? Please be part of within the dialogue beneath.

Have a tip for CleanTechnica? Wish to promote? Wish to recommend a visitor for our CleanTech Speak podcast? Contact us right here.

CleanTechnica Vacation Want Guide

Click on to obtain.

Our Newest EVObsession Video

I do not like paywalls. You do not like paywalls. Who likes paywalls? Right here at CleanTechnica, we carried out a restricted paywall for some time, however it all the time felt unsuitable — and it was all the time powerful to determine what we must always put behind there. In idea, your most unique and greatest content material goes behind a paywall. However then fewer folks learn it!! So, we have determined to utterly nix paywalls right here at CleanTechnica. However…

Thanks!

Commercial

CleanTechnica makes use of affiliate hyperlinks. See our coverage right here.

{kind=link}