Nio’s gross margin will probably be underneath stress as a consequence of decrease deliveries, however stronger execution is beginning to present up, which might assist car margins get well within the second half, based on Deutsche Financial institution.

Nio (NYSE: NIO) is anticipated to report second-quarter earnings later this month, with an actual date but to be introduced. As standard, Deutsche Financial institution analyst Edison Yu’s group shared their preview.

Nio’s gross margin will stay underneath stress as its gross sales quantity declined within the second quarter, however the firm’s stronger execution is beginning to present, the group stated in a analysis notice titled “Blue Sky Rising” despatched to traders immediately.

Beforehand launched knowledge confirmed that Nio delivered 23,520 autos within the second quarter, barely above the decrease finish of its steerage vary of 23,000 to 25,000 autos. This was down 6.14 p.c year-on-year and down 24.23 p.c from the primary quarter.

Nio had beforehand guided whole income for the second quarter to be between RMB 8.742 billion ($1.27 billion) and RMB 9.37 billion, a lower of about 15.1 p.c to 9.0 p.c from the identical quarter in 2022.

Yu’s group expects Nio to report income of RMB 9.1 billion within the second quarter, which is in keeping with consensus estimates.

Nio’s gross margins will probably be underneath stress as a consequence of decrease deliveries and may very well be round 2 p.c to three p.c within the second quarter, the group stated, including that they anticipate the corporate’s car margins might present small sequential enchancment.

Whereas working bills have been a lot decrease than anticipated within the first quarter, promoting, common and administrative bills (SG&A) ought to improve quarter-on-quarter as Nio aggressively promoted new fashions, the group famous.

“All this interprets into one other large loss (-2.86 EPS) and money burn which is properly understood by the market,” the group wrote.

As a backdrop, Nio reported income of RMB 10.68 billion within the first quarter, beneath the decrease finish of its steerage vary of RMB 10.93 billion to RMB 11.54 billion, though first-quarter car deliveries have been throughout the steerage vary.

Nio’s gross margin within the first quarter was 1.5 p.c, a brand new low because the first quarter of 2020, down from 3.9 p.c within the fourth quarter of 2022.

Regardless of the weak first half, Nio’s stronger execution is beginning to present.

“Following a file July the place Nio delivered >20,000 autos for the primary time, we anticipate 3Q23 steerage to be >60,000, pushed by wholesome ES6 order ebook (not less than 50% of combine),” Yu’s group wrote.

ET5 Touring and ES8 are additionally rising quickly, the group stated, including that they anticipate Nio’s deliveries to develop sequentially within the fourth quarter with the assistance of the brand new EC6.

Nio administration had beforehand talked about that they anticipate car margins to return to double digits within the third quarter and over 15 p.c within the fourth quarter. The corporate had a car margin of 5.1 p.c within the first quarter.

Primarily based on the elements outlined by Nio administration, this seems to be achievable, though the complete influence of the advantages will not be seen till subsequent 12 months, Yu’s group stated.

SG&A will rise sequentially within the second quarter as a consequence of increased advertising bills, however as a share of gross sales within the second half of the 12 months it ought to fall sharply, based on the group.

As well as, money burn will naturally enhance within the second half as a consequence of good working capital and capex will probably be near flat year-on-year or about $7 billion, the group stated.

Nio noticed file deliveries in July, and order consumption ought to stay wholesome within the coming quarters, pushed largely by ES6, the group famous.

On the similar time, opex and capex will probably be extra managed as Nio cuts spending on non-core initiatives.

Taking all these elements into consideration, the group raised their forecast for Nio’s deliveries in 2023 by 10,000 models to 180,000 models and raised gross margins by 40 foundation factors to 7.4 p.c.

For 2024, the group raised their supply forecast for Nio from 270,000 models to 285,000 models and raised their forecast for gross margin from 13.7 p.c to 13.9 p.c.

The changes to those parameters resulted within the group elevating their value goal on Nio to $17 from the unique $13. The group maintained its Purchase ranking on Nio.

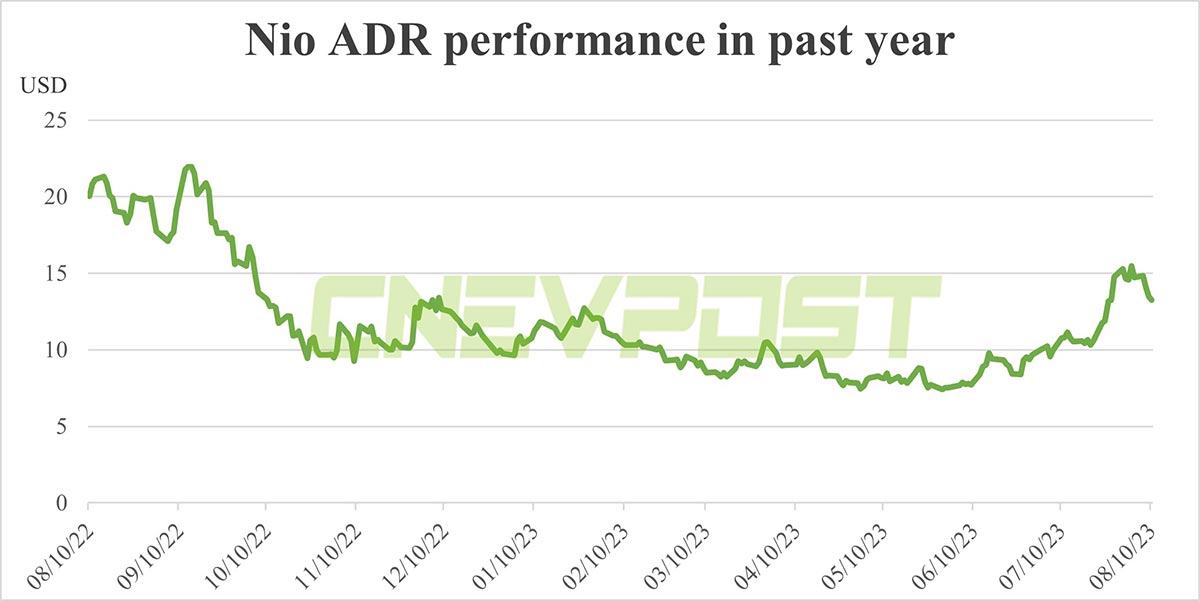

Nio closed down 1.56 p.c to $13.25 within the US inventory market yesterday, and the value goal implies a 28 p.c upside.

“Positioning-wise, we expect the inventory can lastly recapture momentum after being a relative laggard all 12 months and in addition see some small potential for strategic optionality,” the group wrote.

CnEVPost needs to re-emphasize that the changes Wall Avenue analysts make to the value goal are the results of their tweaking of a handful of parameters in complicated valuation fashions.

Subsequently, it’s extra essential to concentrate to why these high minds on this planet are adjusting the parameters of their fashions than to the modifications within the value goal.

{kind=link}